Defining AI 402 pay in tax terms

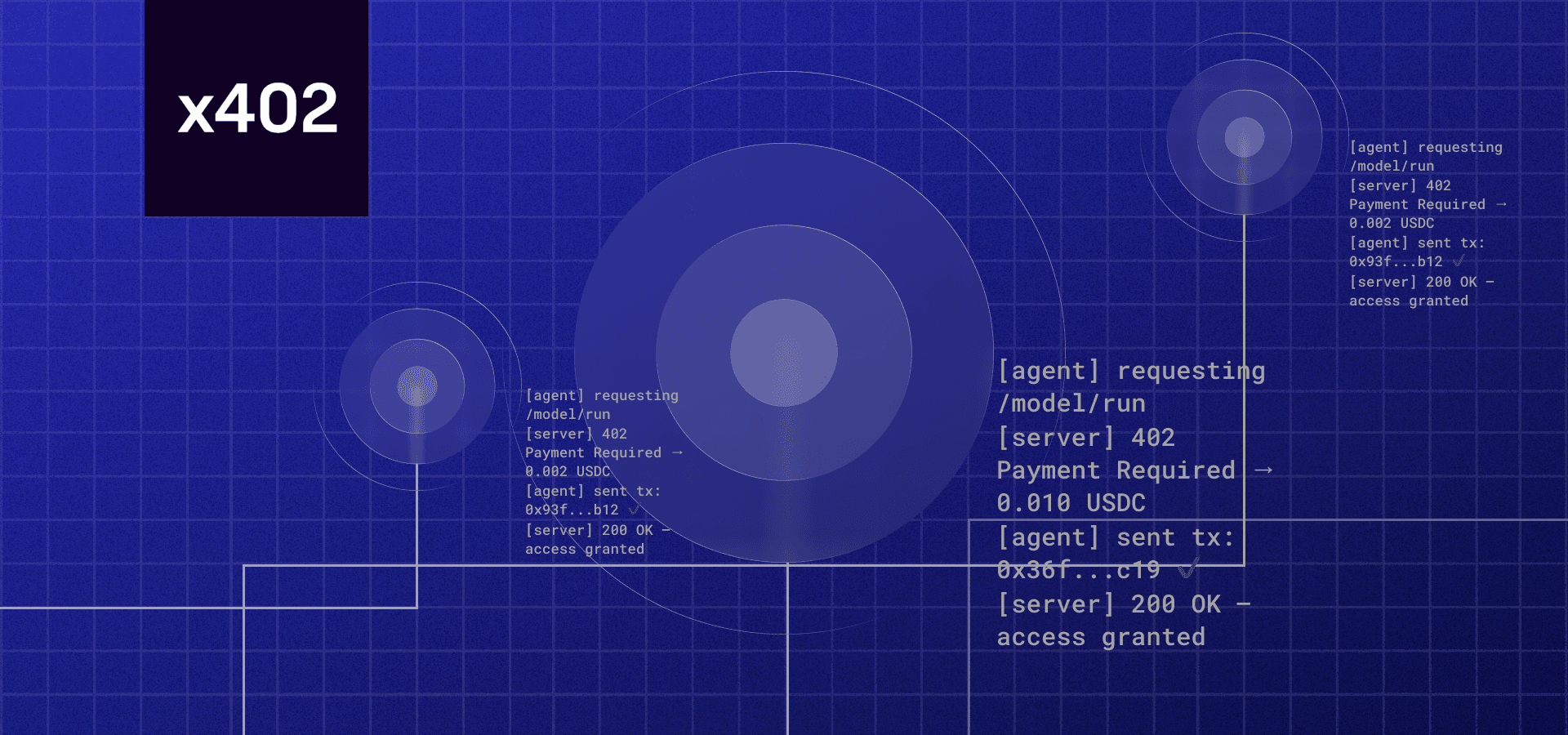

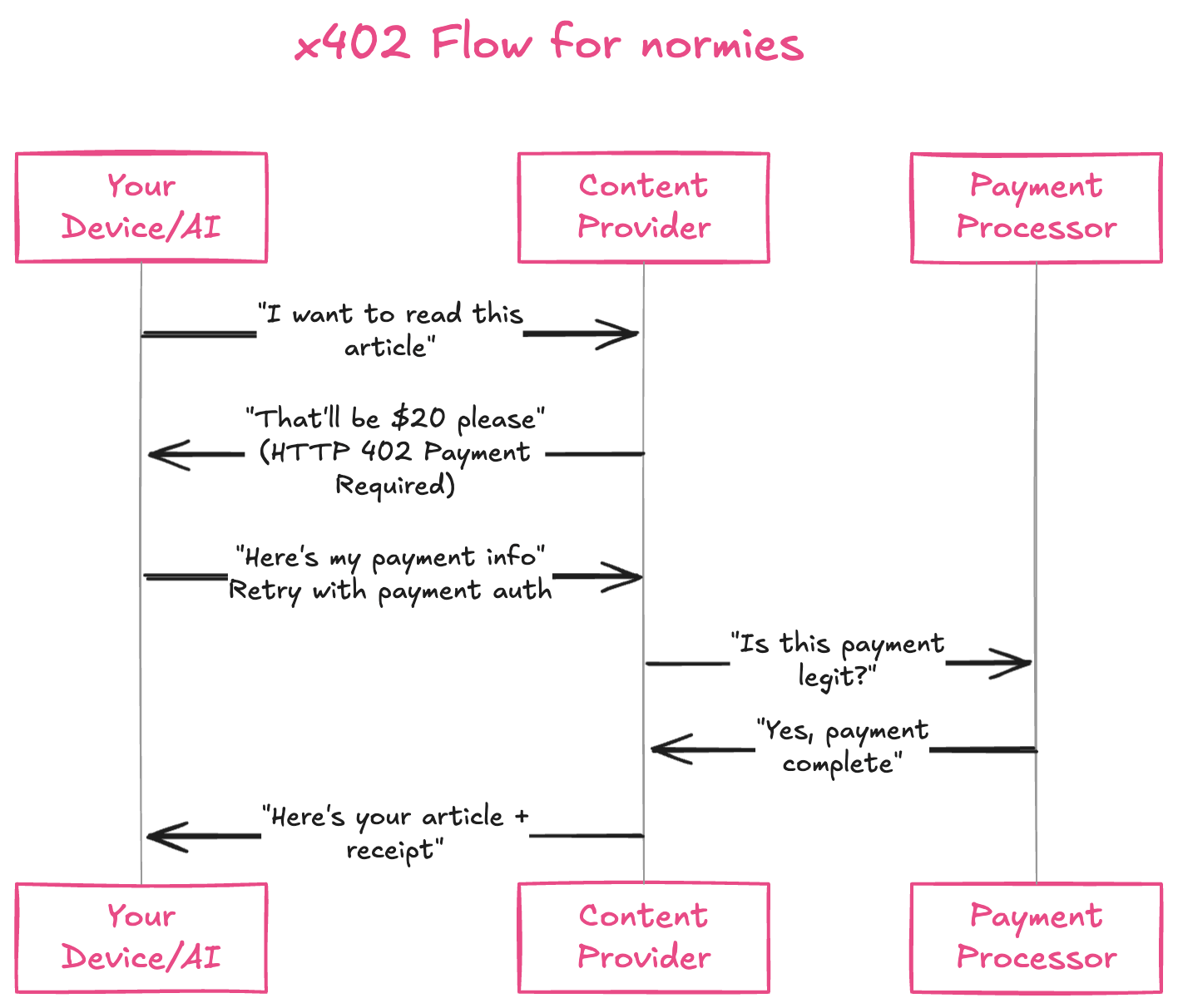

The term "AI 402 pay" refers to transactions executed via the x402 protocol, a technical standard for autonomous machine-to-machine micropayments. Developed by Coinbase and released as open-source software in 2025, the protocol revives the HTTP 402 status code to enable instant crypto settlements between AI agents. This infrastructure allows digital agents to hold funds in agent wallets and transact autonomously, subject to budget rules set by their human owners.

From a regulatory perspective, these transactions are not a new asset class but rather exchanges of existing digital assets. Current IRS guidance treats cryptocurrency as property, meaning every autonomous payment triggered by an AI agent constitutes a taxable event. Whether the transaction is classified as income, an expense, or a property exchange depends on the specific nature of the service or data exchanged, not the automation of the payment rail.

Because the x402 protocol is open source, its underlying mechanics are transparent and publicly auditable. This transparency is critical for tax compliance, as it provides a verifiable ledger of autonomous transactions. Taxpayers must track these micropayments with the same rigor applied to traditional cryptocurrency trades, ensuring that the fair market value at the time of each autonomous transaction is recorded for reporting purposes.

Comparing payment rails for tax reporting

Use this section to make the AI 402 Pay decision easier to compare in real life, not just on paper. Start with the reader's actual constraint, then separate must-have requirements from details that are merely nice to have. A practical choice should survive normal use, maintenance, timing, and budget. If a recommendation only works in an ideal situation, call that out plainly and give the reader a fallback path.

| Factor | What to check | Why it matters |

|---|---|---|

| Fit | Match the option to the primary use case. | A good deal still fails if it does not fit the job. |

| Condition | Verify age, wear, and service history. | Hidden condition issues erase upfront savings. |

| Cost | Compare purchase price with likely upkeep. | The cheapest option is not always the lowest-cost option. |

IRS stance on cryptocurrency and digital assets

Use this section to make the AI 402 Pay decision easier to compare in real life, not just on paper. Start with the reader's actual constraint, then separate must-have requirements from details that are merely nice to have. A practical choice should survive normal use, maintenance, timing, and budget. If a recommendation only works in an ideal situation, call that out plainly and give the reader a fallback path.

The simplest way to use this section is to write down the must-have criteria first, then compare each option against those criteria before weighing nice-to-have features.

Compliance Checklist for AI Agent Billing

Integrating x402 payments introduces distinct tax reporting obligations because these transactions are treated as taxable events involving digital asset property. Under current IRS guidance, any exchange of cryptocurrency for services or goods triggers capital gains or losses that must be calculated and reported. Businesses must implement rigorous tracking systems to capture the fair market value of digital assets at the exact moment of each autonomous transaction.

The x402 protocol’s open-source nature allows for transparent verification of these transactions, which can simplify the audit trail. However, the burden of accurate reporting remains with the business entity. By adhering to these steps, organizations can maintain compliance while leveraging the efficiency of autonomous agent billing.

Frequently asked questions on AI 402 tax rules

The following questions address common queries regarding the tax implications of autonomous agent transactions under current regulations. These responses reflect existing legal frameworks and official documentation regarding digital asset transactions.

No comments yet. Be the first to share your thoughts!