Ai payment fraud detection budget

AI-Driven Payment Fraud Prevention works best when the purchase path is explicit. Verify the source, compare the offer against real alternatives, check the total cost, and confirm what happens after payment before you decide. After each comparison, write down the one risk that would change your mind. If the seller, condition, support, warranty, shipping, or upkeep still feels uncertain, resolve that question before moving to checkout.

The simplest way to use this section is to verify the seller, compare the total cost, and resolve the biggest risk before you commit.

Shortlist real options

Use this section to make the AI-Driven Payment Fraud Prevention decision easier to compare in real life, not just on paper. Start with the reader's actual constraint, then separate must-have requirements from details that are merely nice to have. A practical choice should survive normal use, maintenance, timing, and budget. If a recommendation only works in an ideal situation, call that out plainly and give the reader a fallback path.

| Factor | What to check | Why it matters |

|---|---|---|

| Fit | Match the option to the primary use case. | A good deal still fails if it does not fit the job. |

| Condition | Verify age, wear, and service history. | Hidden condition issues erase upfront savings. |

| Cost | Compare purchase price with likely upkeep. | The cheapest option is not always the lowest-cost option. |

Inspect the expensive parts

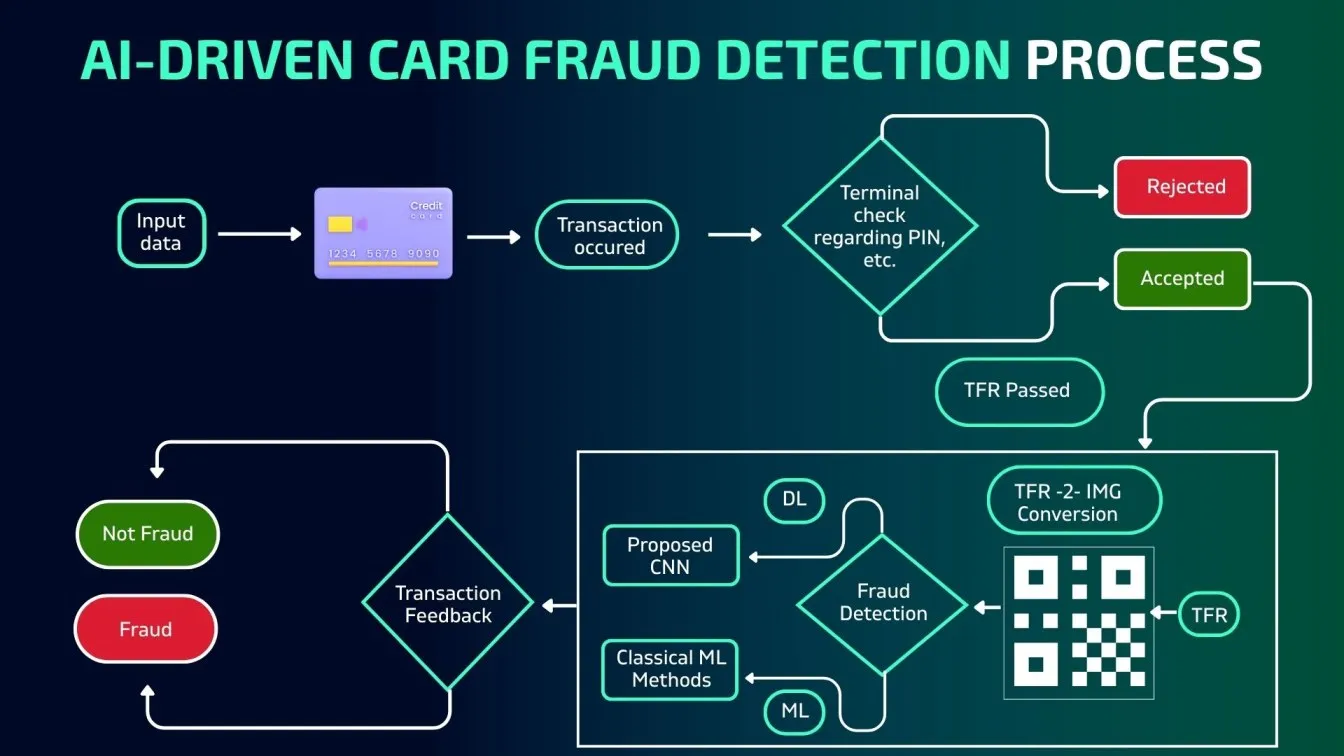

Fraud prevention software is only as good as its configuration. A misconfigured rule set can block legitimate customers or let high-value transactions slip through. Before committing to a platform, run through these five checks to ensure the system handles the most costly failure points effectively.

AI fraud detection must happen in milliseconds. If the analysis adds more than 500ms to the checkout flow, you lose customers to cart abandonment. Test the system under peak load to ensure it maintains speed without skipping steps.

Blocking legitimate transactions is expensive. Look for platforms that use machine learning to distinguish between unusual but valid behavior and actual fraud. A good system reduces false positives by 30-50% compared to static rules, saving revenue and customer trust.

Basic IP checks are no longer enough. Ensure the tool analyzes device fingerprinting, mouse movements, and typing patterns. These behavioral signals help identify account takeovers and synthetic identity fraud that static data misses.

Your fraud tool must talk to your payment gateway and CRM seamlessly. Look for pre-built connectors for Stripe, PayPal, and major e-commerce platforms. Deep integration allows for automatic refunds and customer notifications, reducing manual workload.

AI isn't perfect. The best systems flag high-risk transactions for human review rather than auto-declining them. This hybrid approach ensures that complex cases get expert attention while automated systems handle routine checks.

As an Amazon Associate, we may earn from qualifying purchases.

Plan for ownership costs

Buying a fraud prevention platform is the first step; keeping it running is where the real budget lives. AI-driven systems are not set-and-forget tools. They require continuous tuning to adapt to new fraud tactics and changing customer behaviors. If you neglect maintenance, the system’s accuracy drops, leading to higher false positives that frustrate legitimate customers and increase operational overhead.

Beyond the software license, expect costs for data infrastructure and specialized talent. Machine learning models need high-quality, labeled transaction data to function correctly. This often means investing in data engineering resources to clean and normalize payment streams. Additionally, you will need analysts who understand both the algorithm’s outputs and the nuances of payment fraud to interpret alerts and adjust thresholds.

The cheapest option rarely wins in the long run. A low-cost solution may lack the real-time processing capabilities or the sophisticated behavioral analysis needed to catch modern fraud. This can lead to significant chargeback losses and reputational damage that far exceed the initial savings. When evaluating platforms, look beyond the sticker price and consider the total cost of ownership, including implementation, training, and ongoing support.

As an Amazon Associate, we may earn from qualifying purchases.

Investing in a robust solution pays for itself by reducing manual review work and preventing fraudulent transactions before they settle. Look for platforms that offer transparent pricing models and clear ROI metrics. This helps you justify the expense to stakeholders and ensures you are getting value for your investment.

Ai payment fraud detection 2026: what to check next

As AI-driven fraud schemes become more sophisticated in 2026, businesses need practical answers to common concerns about implementation and workforce impact.

Will fraud investigators be replaced by AI?

Experienced analysts often recognize subtle behavioral patterns that automated systems might overlook. These human insights remain a critical component of effective fraud prevention. The role of AI, therefore, is not replacing fraud professionals but amplifying their capabilities across the stack.

How does AI reduce false positives in transaction monitoring?

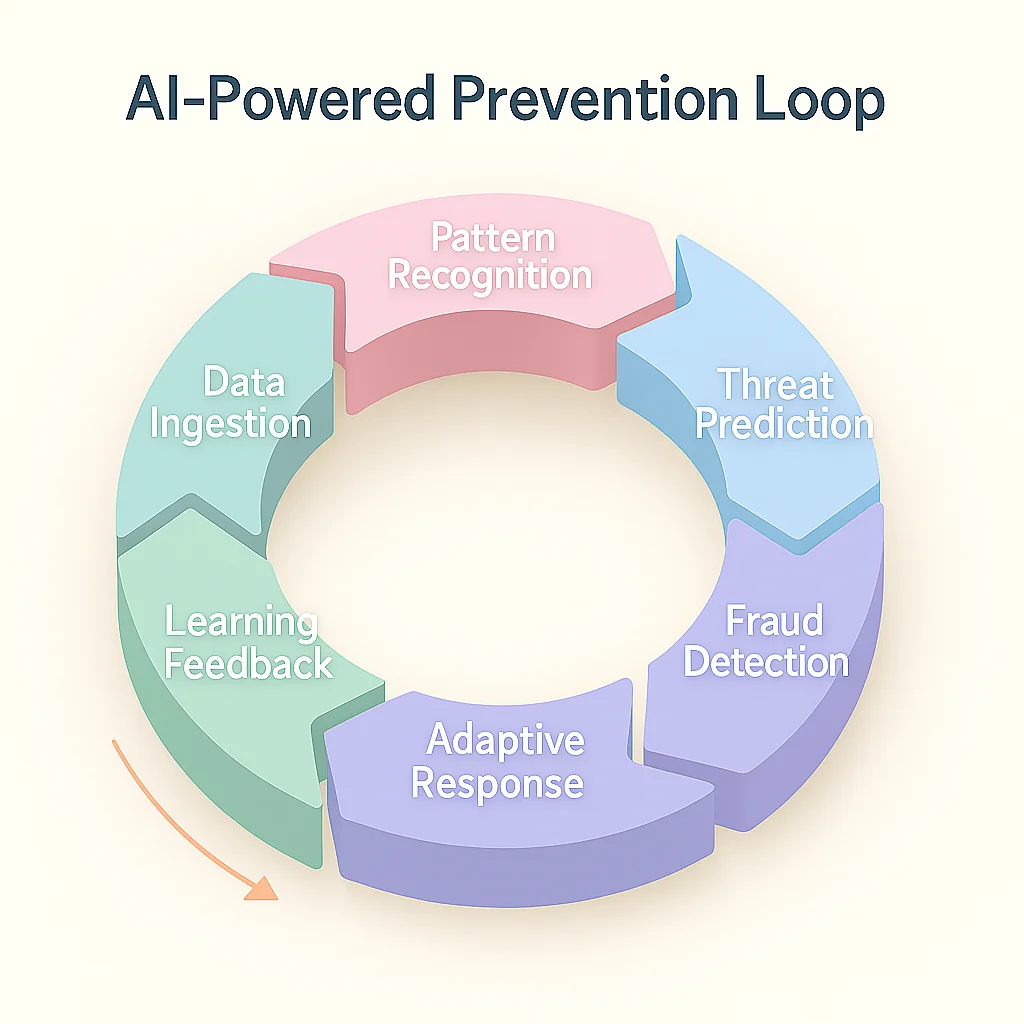

AI models analyze transaction data in real time to distinguish between legitimate unusual activity and actual fraud. By learning from historical data and continuous feedback loops, these systems reduce false positives, increase approval rates, and improve the overall customer experience.

What are the main challenges of implementing AI fraud detection?

Financial institutions must pivot from static, rule-based systems to dynamic AI models. Key challenges include ensuring data quality, integrating with existing payment infrastructure, and managing the ethical implications of automated decision-making while maintaining regulatory compliance.

How quickly can AI detect new fraud patterns?

Unlike traditional systems that rely on predefined rules, AI-powered fraud detection uses machine learning to identify emerging threats. As AI-driven fraud campaigns grow more coordinated and cross-channel, these systems adapt quickly to new tactics, helping institutions stay ahead of evolving risks.

No comments yet. Be the first to share your thoughts!