Set up the data pipeline

Building an effective AI payment fraud detection system starts with a robust data pipeline. This pipeline acts as the central nervous system, ingesting raw transaction data and preparing it for real-time analysis. Without clean, structured data, even the most advanced machine learning models will fail to identify fraudulent activity.

1. Ingest raw transaction streams

The first step is capturing high-volume transaction data from payment gateways, banks, and merchant acquirers. This data must be ingested in real time to enable immediate analysis. J.P. Morgan highlights how AI can automate payment validation screening, but this requires a steady, low-latency feed of transaction details including amount, timestamp, and merchant category.

2. Enrich with device and behavioral signals

Raw transaction data is rarely enough to detect sophisticated fraud. You must enrich each event with contextual signals. This includes device fingerprinting, IP geolocation, and user session history. Velocity checks—monitoring how frequently a user initiates transactions—are critical here. If a single device ID triggers multiple high-value purchases in minutes, the system flags it immediately.

3. Normalize and standardize formats

Different payment processors use different data schemas. To train accurate models, you must normalize these inputs into a unified format. This step ensures that the AI sees consistent features, such as standardizing currency codes, timestamp formats, and merchant IDs. Emburse notes that AI fraud detection relies on machine learning models analyzing this structured data to identify patterns that humans might miss.

4. Validate data quality and completeness

Before data enters the model, it must pass quality checks. Missing fields, outliers, or corrupted records can skew predictions. Implement automated validation rules to filter out noise. For example, reject transactions with invalid card numbers or mismatched billing addresses before they reach the decision engine. This reduces computational load and improves model accuracy.

5. Route to the decision engine

Once enriched and validated, the data is routed to the real-time decision engine. This component applies the trained AI models to score each transaction. Scores are then used to approve, decline, or flag transactions for manual review. The entire process must happen in milliseconds to avoid disrupting the user experience.

Train the machine learning models

Before an AI system can spot fraud, it must learn what normal behavior looks like. This happens during the training phase, where developers feed historical transaction data into machine learning algorithms. The model scans millions of past records to find patterns that distinguish legitimate purchases from suspicious activity. Without this foundation, real-time monitoring would be blind to the subtle shifts in how fraudsters operate.

The training process relies on specific techniques to identify anomalies. Velocity checks analyze the speed and frequency of transactions, flagging accounts that suddenly spike in activity. Device fingerprinting tracks unique digital signatures, such as browser configurations or IP addresses, to detect when a legitimate account is accessed from an unfamiliar device. These methods allow the model to build a complex profile of each user’s typical behavior.

Financial institutions like Mastercard and J.P. Morgan have invested heavily in refining these models. They use large datasets to ensure the AI can handle the vast volume of global transactions while minimizing false positives. The goal is to create a system that adapts quickly to new fraud tactics without disrupting the experience for honest customers. This continuous learning loop is essential for staying ahead of increasingly sophisticated criminal networks.

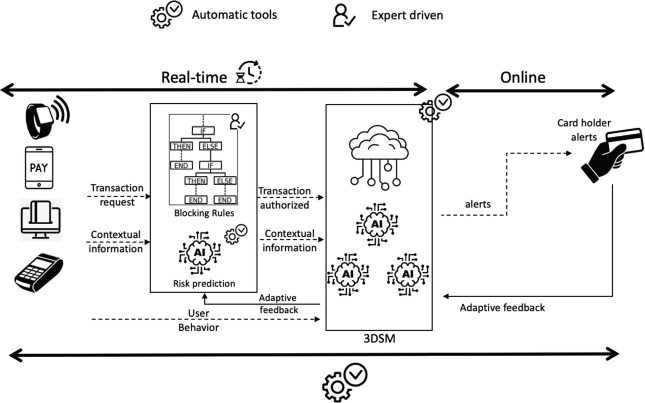

Configure real-time transaction rules

Setting up dynamic rules is the backbone of real-time payment fraud detection. Instead of relying on static, black-and-white lists that block legitimate customers, you configure systems to evaluate transactions against multiple signals simultaneously. This approach, supported by Mastercard, allows banks to reduce false positives while catching sophisticated attacks.

Start with velocity checks. These rules monitor the frequency of transactions from a single account or device within a specific time window. If a card is used three times in different countries within an hour, the system flags it immediately. This simple heuristic stops many basic carding attempts before they process.

Next, implement device fingerprinting. By analyzing the hardware and software characteristics of the user’s device, you can detect when a transaction originates from a known fraud tool or a mismatched environment. J.P. Morgan notes that combining device data with behavioral biometrics creates a robust layer of verification that is difficult for bots to spoof.

Finally, integrate geolocation anomalies. If a transaction occurs far from the user’s last known location or typical spending zone, apply stricter verification steps. These dynamic rules work together to create a real-time monitoring environment that adapts to emerging threats without manual intervention.

Connect your AI system to payment gateways

Integrating an AI fraud detection layer with existing payment processors like Stripe, PayPal, or 402-compliant gateways requires a two-way data pipeline. The goal is to intercept transactions before they settle, allowing your AI model to analyze patterns in real-time. This process relies on specific techniques like velocity checks and device fingerprinting to flag suspicious activity instantly.

Configure your payment gateway to send webhook events for every transaction attempt. These webhooks must carry essential metadata, including IP address, device ID, and transaction velocity. J.P. Morgan notes that AI-powered validation screening significantly reduces fraud by processing this data automatically before approval. Source: J.P. Morgan

Pass device-specific signals from the webhook payload to your AI engine. Device fingerprinting identifies unique hardware and browser characteristics, helping detect when a single device is generating multiple fraudulent accounts. This data point is critical for distinguishing between legitimate new users and coordinated fraud rings.

Set strict velocity limits within your integration logic. If a single card or IP address exceeds a defined number of attempts within a short window, the AI system should automatically flag or block the transaction. This prevents brute-force attacks and rapid-fire testing of stolen credentials.

Your gateway integration must handle asynchronous responses from the AI model. Once the AI analyzes the fingerprint and velocity data, it returns a decision (approve, decline, or review). Update the transaction status in your database accordingly and notify the user if further verification is needed.

This integration transforms your payment gateway from a simple processor into an intelligent security checkpoint. By leveraging real-time data and AI-driven insights, you can significantly reduce false positives while catching sophisticated fraud attempts.

Monitor and adjust model performance

AI fraud detection is not a set-it-and-forget-it system. It requires continuous monitoring to ensure velocity checks and device fingerprinting remain effective against evolving threats. Without regular adjustments, models drift, leading to higher false positives that frustrate customers or false negatives that allow fraud through.

Start by reviewing false positives and false negatives weekly. A false positive occurs when a legitimate transaction is blocked, while a false negative lets a fraudulent one pass. Analyze these cases to identify patterns. For instance, if velocity checks are flagging too many legitimate high-volume merchants, adjust the thresholds. If device fingerprinting misses new spoofing techniques, update the detection rules.

Next, retrain the models with fresh data. Incorporate the latest transaction logs and fraud reports to keep the AI sharp. Mastercard and J.P. Morgan emphasize that continuous learning is essential for resilience. By feeding new examples into the system, the AI adapts to new fraud tactics before they become widespread.

Finally, establish a monthly review cycle. Use the checklist below to ensure all components are aligned.

-

Review false positive and false negative rates

-

Adjust velocity check thresholds based on merchant feedback

-

Update device fingerprinting rules for new spoofing methods

-

Retrain models with the latest transaction data

-

Document all changes and their impact on fraud detection

No comments yet. Be the first to share your thoughts!