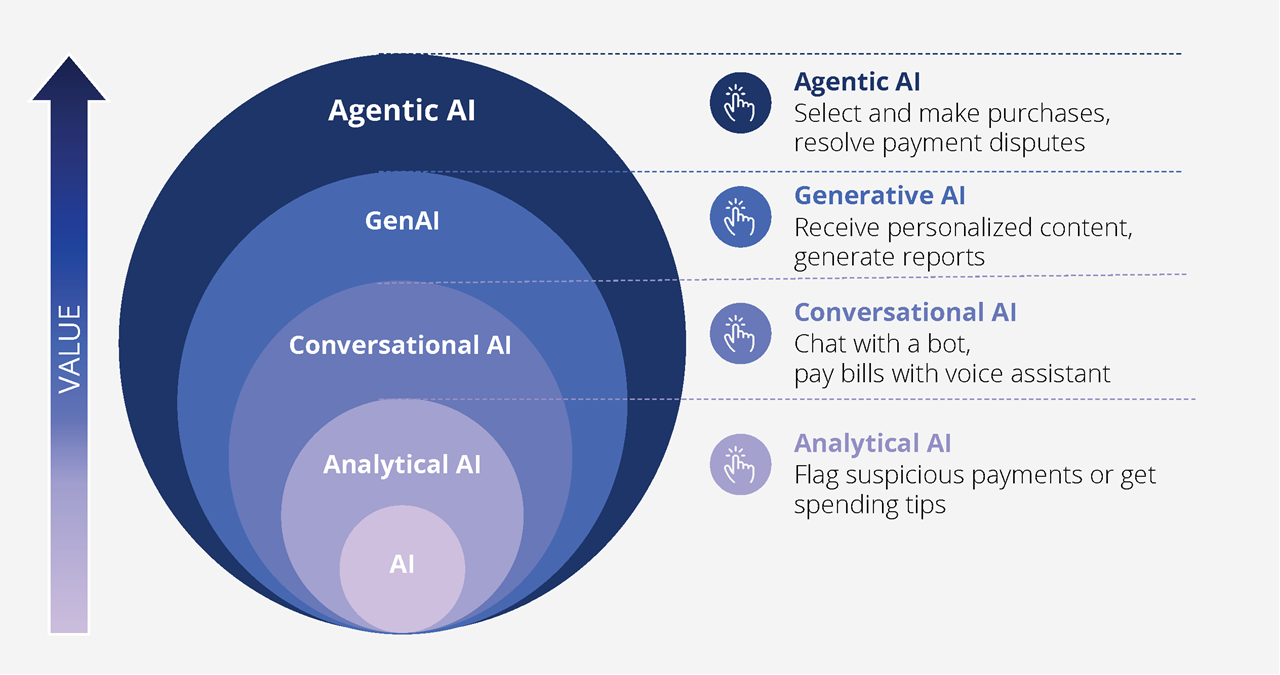

What AI payment optimization actually does

AI payment optimization is not a marketing term for automated email replies or basic chatbots. It is a backend engine that makes real-time decisions on every transaction. While simple automation follows rigid, pre-set rules, AI payment optimization uses machine learning to analyze data as it happens, adjusting routing, fraud checks, and pricing to maximize success.

The core difference lies in adaptability. Traditional systems rely on static logic: if a transaction fails once, it is blocked forever. AI payment optimization treats each transaction as unique. It evaluates hundreds of signals—device fingerprint, geolocation, historical behavior—and adjusts the decision path instantly. This dynamic approach allows payment teams to analyze complex data patterns and uncover revenue opportunities that static systems miss.

This capability spans three critical areas: transaction routing, fraud detection, and authorization rates. By optimizing these elements simultaneously, businesses can improve payment performance without increasing risk. According to industry analysis, AI in payments refers specifically to the use of machine learning to optimize these areas in real time, moving beyond simple rule-based filtering to intelligent, predictive decisioning 1.

Step 1: Audit your current payment stack

Before deploying AI payment optimization, you must understand where your current infrastructure is leaking revenue. AI is an engine, not a foundation; it cannot fix a broken engine, but it can make a good one run significantly faster. Your first task is to map the entire payment journey, from the initial transaction request to the final settlement, to identify specific failure points.

Identify decline rates and fraud friction

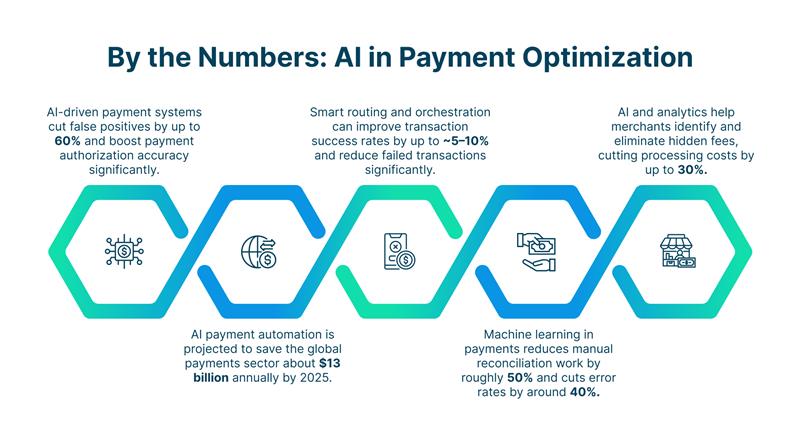

Start by analyzing your decline logs. A high decline rate often signals routing inefficiencies or overly aggressive fraud filters that reject legitimate transactions. According to industry analysis from Checkout.com, understanding these decline reasons is the first step in optimizing payment conversion. You need to distinguish between hard declines (invalid card details) and soft declines (insufficient funds or issuer blocks), as AI strategies for each differ significantly. High fraud friction that rejects good customers is just as costly as fraud losses themselves.

Evaluate routing and processor performance

Next, assess how your transactions are being routed. Are you sending traffic to the most cost-effective or highest-approval processors for each card type and region? Payment orchestration platforms can provide insights into this, as noted in recent coverage by BridgerPay on how AI transforms payment orchestration. Without a clear view of which acquirers are performing best for your specific customer base, you are likely overpaying on interchange fees or losing sales to suboptimal routing.

Calculate the cost of inefficiency

To quantify the impact of these issues, use the calculator below. It estimates the annual revenue leakage caused by current decline rates and routing inefficiencies. This figure helps justify the investment in AI optimization by showing the tangible gap between your current performance and potential revenue.

This audit provides the baseline data needed for the next steps. Once you know exactly where the leaks are, you can configure your AI tools to target those specific inefficiencies with precision.

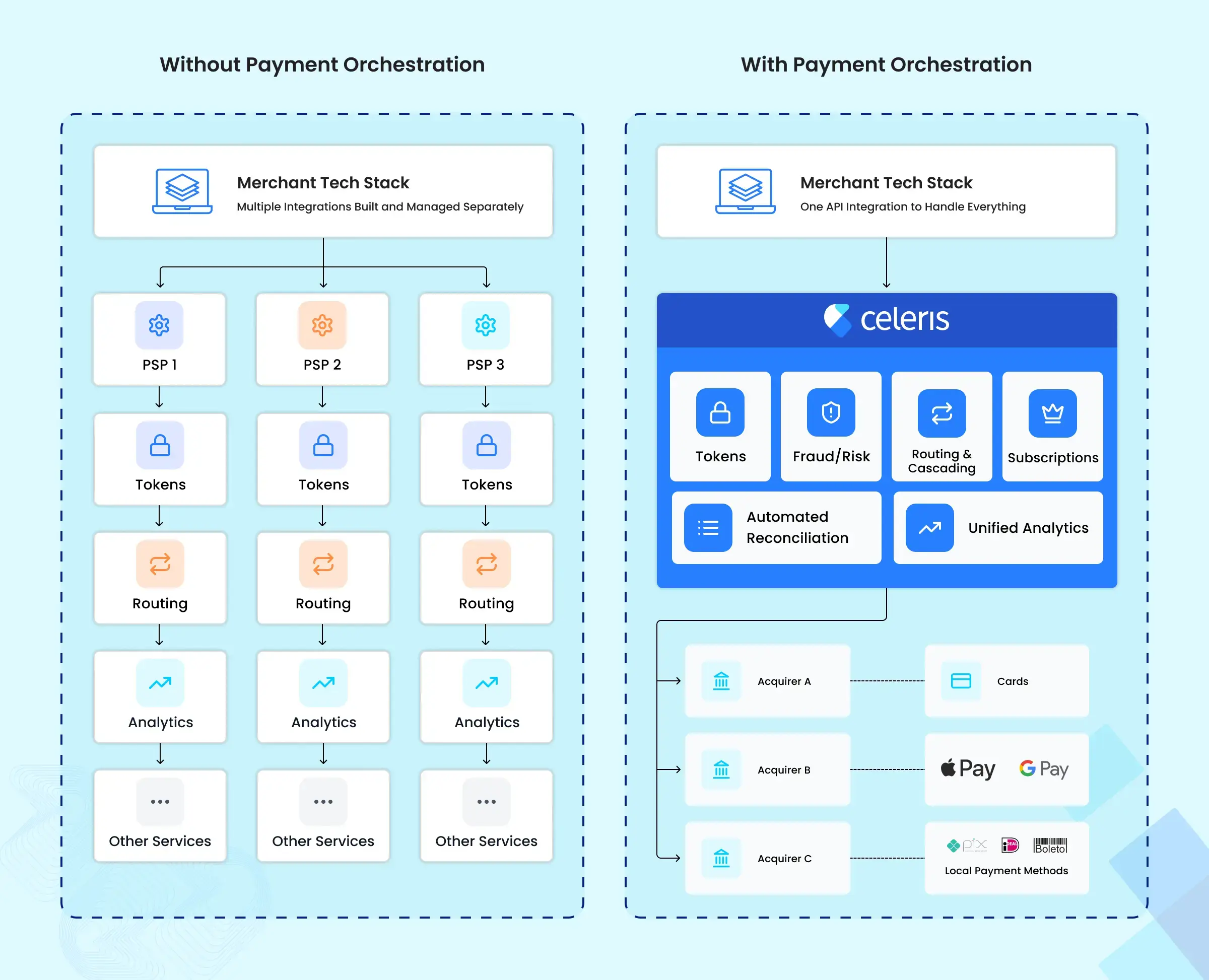

Step 2: Choose the right orchestration layer

Selecting a payment orchestration layer is the structural decision that determines whether your AI initiatives scale or stall. Unlike a simple gateway, an orchestration platform sits between your checkout and multiple payment service providers (PSPs), managing the flow of transaction data. For AI-driven routing to work effectively, this layer must expose real-time APIs and support dynamic decisioning logic.

The ideal platform acts as a central nervous system. It collects performance data from every processor and uses machine learning to route each transaction to the cheapest, highest-approval provider at that exact moment. This requires a system that can handle complex rules without requiring custom code for every change.

When evaluating options, focus on three core capabilities: AI-powered fee intelligence, multi-provider redundancy, and seamless integration ease. Leading providers like Stripe and Adyen have built these capabilities directly into their suites, while specialized orchestration firms offer more granular control over routing logic.

The table below compares how major players approach AI orchestration. Stripe offers a managed, all-in-one suite with built-in intelligence, while Adyen provides a global network with advanced risk and conversion optimization. Specialized orchestration platforms like Bridge or Vindicia focus on complex routing rules and multi-provider redundancy.

| Provider | AI Capability | Routing Flexibility | Integration Ease |

|---|---|---|---|

| Stripe | Payments Intelligence Suite (automated decisions) | High (multi-provider support) | Very High (native SDKs) |

| Adyen | Uplift (conversion & risk optimization) | High (global network) | High (unified platform) |

| Bridge | Smart Routing (rule-based + ML) | Very High (multi-PSP) | Medium (API-first) |

| Vindicia | Chargeback & Recovery AI | High (fallback logic) | Medium (API-first) |

Step 3: Configure dynamic fraud and pricing rules

Setting up AI payment optimization requires balancing two competing forces: strict fraud detection and smooth customer conversion. When you configure dynamic rules, the system evaluates each transaction in real time, adjusting its response based on risk scores. This approach moves beyond static blocklists, allowing legitimate customers to pass through while intercepting suspicious activity before it impacts your bottom line.

Align fraud decisions with performance goals

AI-driven fraud solutions work best when they are tuned to align with specific business objectives. Instead of simply declining high-risk scores, the system can route transactions to secondary verification methods, such as 3D Secure authentication or manual review. This ensures that you protect transactions without sacrificing the customer experience. Mastercard notes that by using AI to align fraud decisions with performance goals, merchants can protect transactions without sacrificing customer experience. This balance is critical for maintaining authorization rates while reducing chargebacks.

Apply dynamic pricing to high-risk transactions

Another powerful feature is the ability to apply dynamic pricing or friction to high-risk transactions. If a transaction scores moderately high on risk, the system might introduce a small additional step, like a one-time password or a quick identity check, rather than a hard decline. This targeted friction helps verify the cardholder's identity without disrupting the flow for low-risk users. It transforms payment optimization from a simple pass/fail gate into a nuanced decision engine that adapts to each user's behavior.

Set clear boundaries for what constitutes low, medium, and high risk. Use historical data to establish baseline decline rates and adjust thresholds based on current fraud trends.

Map out the customer journey for each risk tier. Low-risk transactions should flow instantly, while medium-risk ones trigger secondary checks like 3D Secure.

Run A/B tests to compare the new dynamic rules against your previous static settings. Monitor authorization rates and fraud metrics to fine-tune the AI model.

Estimate revenue impact

Understanding the potential lift from these optimizations helps justify the implementation effort. Use the calculator below to estimate how reducing false declines and optimizing routing can impact your revenue.

Monitor, test, and refine AI payment optimization

AI payment optimization is not a one-time configuration; it is a continuous feedback loop. Even the most sophisticated models drift as consumer behavior and fraud tactics evolve. Without active monitoring, your automated routing decisions will gradually lose effectiveness, leading to higher decline rates and lower net revenue.

Establish baseline metrics

Before enabling automated adjustments, define your current performance baselines. Track approval rates, net authorization rates, and fraud loss ratios by payment method and issuer. These metrics serve as the control group for all future tests. Without accurate baselines, you cannot measure the true impact of AI-driven changes. Use your payment processor’s dashboard to export historical data, ensuring you have at least three months of consistent transaction volume for reliable comparison.

Implement A/B testing for routing rules

Never roll out AI changes to 100% of traffic immediately. Use A/B testing to isolate the impact of specific optimization rules. Split your traffic so that one group follows your existing static routing logic, while the other group is processed by the AI model. Monitor the results over two to four weeks to account for weekly spending cycles. This approach prevents a single bad algorithm update from disrupting your entire revenue stream. Stripe’s Payments Intelligence Suite, for example, allows for real-time decisioning that can be tested against legacy rules to verify profit maximization.

Review model performance monthly

Schedule a monthly review of your AI model’s performance. Look for shifts in approval rates across different regions or card networks. If a specific issuer’s approval rate drops unexpectedly, it may indicate a technical issue with that bank’s API rather than a fraud problem. Adjust your routing weights accordingly. Continuous human oversight ensures that the AI remains aligned with your business goals, such as prioritizing customer experience over pure fraud prevention in certain high-value segments. Regular audits prevent the system from optimizing for the wrong outcome.

Update rules based on feedback

Use the data from your A/B tests and monthly reviews to refine your routing rules. If the AI consistently declines a specific type of transaction that your fraud team has deemed low-risk, update the model’s training data to reflect this. Conversely, if the model approves transactions that later result in chargebacks, tighten the fraud thresholds. This iterative process ensures that your AI payment optimization strategy adapts to new threats and opportunities. Treat your payment stack as a living system that requires constant tuning to maintain peak performance.

Common questions about AI payment optimization

Implementing AI payment optimization shifts how teams handle transaction routing and fraud detection. The following questions address the practical concerns of cost, team impact, and technical integration.

No comments yet. Be the first to share your thoughts!